While the unfortunate answer to this question is almost always “more”, I bet we can find some data-backed baselines that make sense.

The general answer that most people will say is “as much as possible.” But when it’s that vague the answer might as well be “nothing.” After all, what is life for if not to enjoy it? Let’s get back to that point later.

Two ways to plan your savings

Saving for specific goals

Suppose you are saving for a specific goal, hallelujah! Our job is fairly simple and it’s a relatively simple math problem. The two numbers we need to know are the amount and time that you want to have the money.

Let’s say you want to plan a wedding in 3 years and expect it to cost $60,000. I am assuming you’re paid monthly. The answer is pretty straightforward:

[months] / [cost] = [$save per month$]

[3 * 12] / $60,000 =

36 / $60,000 = $1,666.67 per monthIt’s fairly simple. This can be applied to any goal. It can become more complex if you plan on investing that money while you save it, such as in a High Yield Savings Account (HYSA), but that’s beyond the scope of this post.

Saving for retirement & other nonspecific goals

If you’ve read the 4% Rule or other retirement calculators, you may have turned your retirement into a specific goal, i.e. one that you know exactly how much money you want to save and how you get there. I highly suggest turning your nonspecific goals into specific goals if you can, especially with retirement.

That said, some people just want “financial security”, and they’re not sure what that means or looks like. In these cases, people talk about savings as a percentage of income.

One of the first financial books I read was back in my teens, The Richest Man in Babylon. This is a great book, I would probably classify it as a fictional Financial Philosophy rather than a pure Financial book that has a strong plan. One of the key points in the book is the pay-yourself-first principle:

“For every ten coins thou placest within thy purse take out for use but nine. Thy purse will start to fatten at once and its increasing weight will feel good in thy hand and bring satisfaction to thy soul.”

George S. Clason, The Richest man in babylon

Here, he is advocating for one-tenth of your earnings, or 10%, should be saved. He is also specifically talking about the financial security, or “satisfaction of thy soul.” I did this for 5-7 years, even while I was paying off debt. It gave me the beginning of a “nest egg” and has been tremendously helpful.

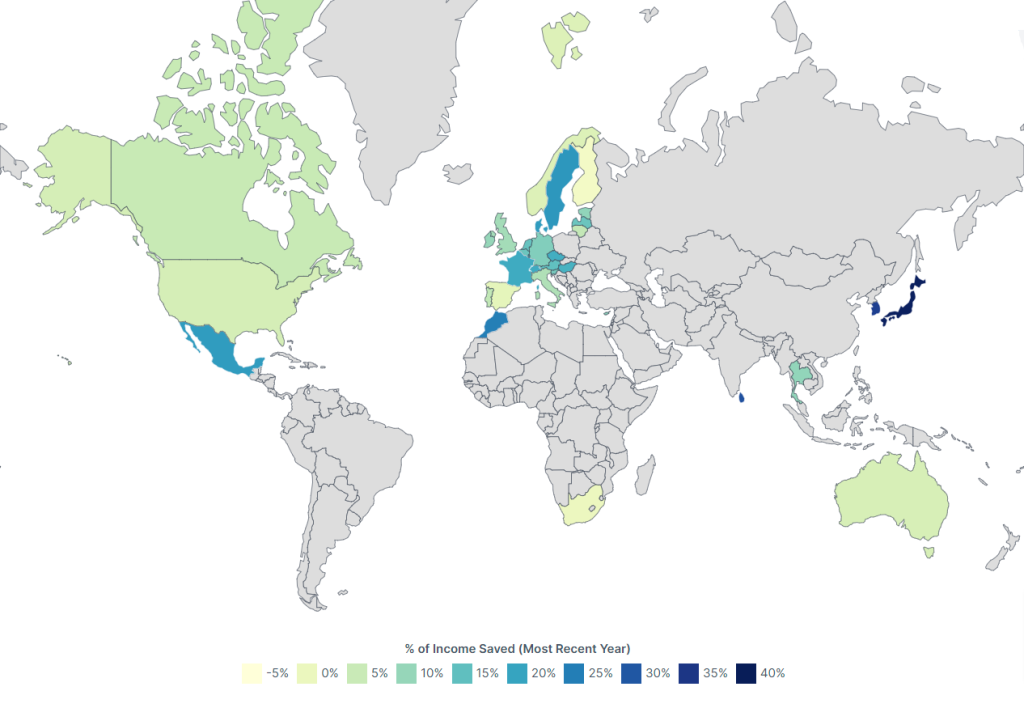

That said, 10% is fairly arbitrary. I also discovered in recent years, that Japan has some of the highest savings rates in the world, around 50%! This number seemed crazy to me. I thought my 10% might be a little bit low, but 50%?

Global income savings rates

I only then found out that the average savings rate in the US is far lower, around 4%.

Here are the rankings as a table.

| Country | % of Income Saved (Most Recent Year) | % of Income Saved (Previous Year) | Data Year |

|---|---|---|---|

| Japan | 39.3% | 54.7% | 2023 |

| South Korea | 33.5% | 33.4% | 2023 |

| Sri Lanka | 30.8% | 29.4% | 2022 |

| Morocco | 24.9% | 26.9% | 2023 |

| Sweden | 21.8% | 12.1% | 2023 |

| Mexico | 21.1% | 20.3% | 2022 |

| Denmark | 21% | 8.5% | 2023 |

| France | 18.8% | 18.2% | 2023 |

| Switzerland | 18.8% | 19.1% | 2021 |

| Czech Republic | 18.2% | 19.4% | 2023 |

| Luxembourg | 18.2% | 24.2% | 2021 |

| Hungary | 17.5% | 15.4% | 2021 |

| Austria | 14.9% | 15.1% | 2023 |

| Netherlands | 14.4% | 17.1% | 2023 |

| Belgium | 13.9% | 10.8% | 2023 |

| Latvia | 13.9% | 14.6% | 2021 |

| Slovenia | 12.9% | 4% | 2023 |

| Germany | 11.9% | 10.7% | 2023 |

| Cyprus | 10.9% | 12.5% | 2021 |

| Estonia | 10.5% | 14.3% | 2021 |

| Thailand | 10.3% | 10% | 2021 |

| Ireland | 10% | 10.1% | 2023 |

| United Kingdom | 8.8% | 9.4% | 2023 |

| Italy | 7.6% | 5.3% | 2023 |

| Portugal | 5.9% | 6.5% | 2023 |

| Lithuania | 5.8% | 12.4% | 2021 |

| Canada | 5.1% | 3.7% | 2023 |

| United States | 3.5% | 4.3% | 2023 |

| Australia | 3.2% | 3.6% | 2023 |

| Norway | 2.4% | 6.4% | 2023 |

| Spain | 0.9% | 14.5% | 2023 |

| Hong Kong | 0.8% | 0.6% | 2023 |

| South Africa | -0.2% | – | 2023 |

| Finland | -1.8% | -1.8% | 2023 |

Why is your saving as a percentage of income important? It’s a fairly easy way to see how well you could do without income.

For instance, if you saved 50% of your income, that means that your expenses are 50% of your income. Therefore, for every month you save 50%, you’ve earned yourself a “free month”. Theoretically, you could work for 6 months of the year and then take off 6 months of the year.

The math breaks out something like this, let’s say you earn $5,000 a month, and you save $2,500 a month and you spend $2,500 a month.

In 6 months, you would have earned $30,000 (6 * $5,000) and spent $15,000 (6 * $2,500). You still have $15,000 that will last you for the next month.

Now, if you’re saving 10%, that means expenses are 90% of your income. You have to save for 9 months to get 1 free month. In the previous example, that means your expenses are $4,500 for every $5,000 you earn.

After 9 months you have earnings of $45,000 (9 * $5,000) and spent $40,500 (9 * $4,500) leaving you with $4,500, one month free.

Now, 50% is a lot. Most people at the beginning of their career won’t be able to do this, and it’s usually only in the later years when your income has increased that you can earn a higher savings rate. This brings us to income as it relates to your age.

Income savings by age

In your earlier years, both your income and your expenses tend to be low. It typically follows that your income will increase as you age, but you need to fight lifestyle inflation (or lifestyle creep). Lifestyle inflation, simply put, is the tendency to spend more money on your life for various niceties, from that extra cup of coffee to buying a Porsche because technically your income covers the payments.

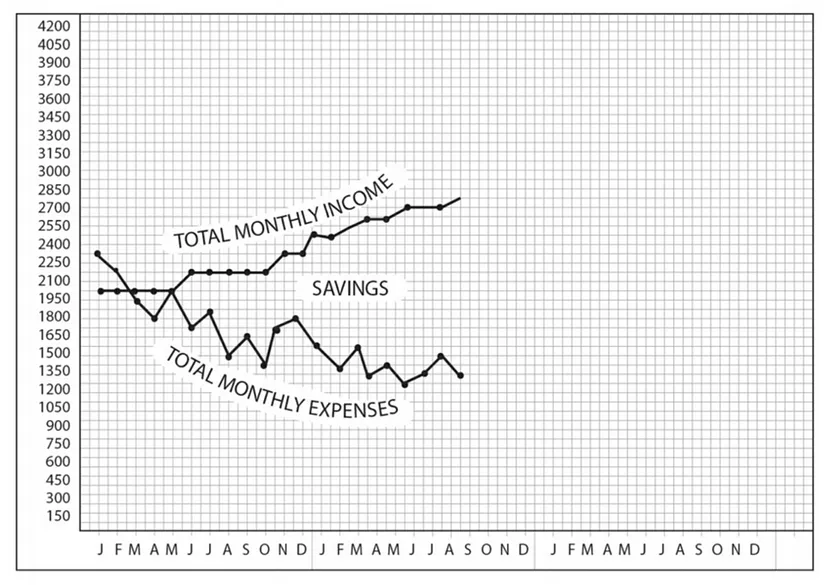

The lower you keep your expenses, the higher your savings rate will be as your income increases. In Your Money Or Your Life, one of the original books about early retirement, they talk about keeping a chart that tracks this exact difference.

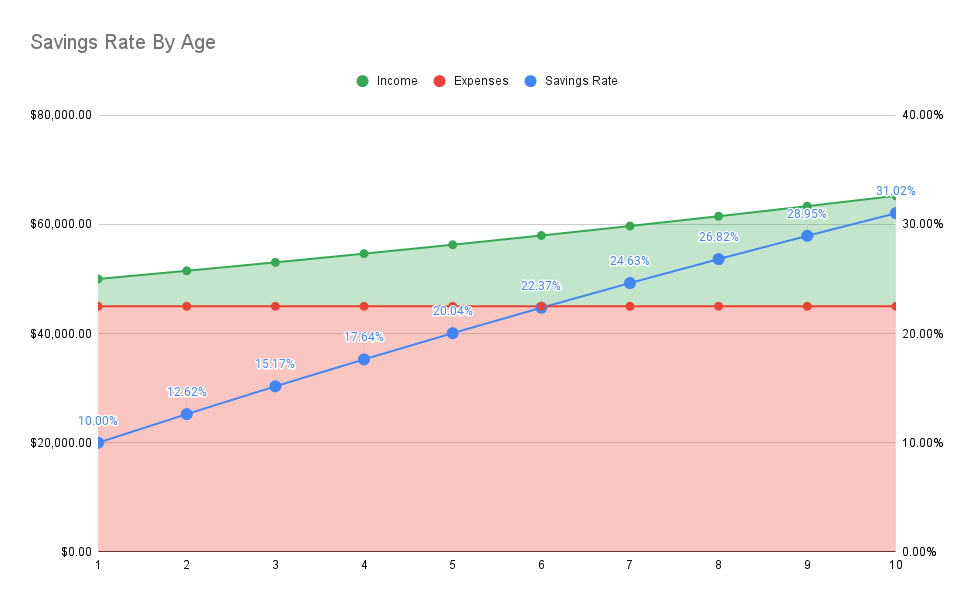

Knowing that your income will increase as age goes on and that if you manage to keep your expenses low, that will also mean your savings rate will increase through age. Let’s say that at 24 you’re earning $50,000 a year and your expenses are $45,000 a year. Assuming that you manage to keep your expenses the same for the next 10 years, but get a 3% boost in your income each year, your savings rate would look like the following:

Here’s the underlying table for this data so you can see how it’s done.

| Year | Income | Expenses | Savings Rate |

|---|---|---|---|

| 1 | $50,000 | $45,000 | 10.00% |

| 2 | $51,500 | $45,000 | 12.62% |

| 3 | $53,045 | $45,000 | 15.17% |

| 4 | $54,636 | $45,000 | 17.64% |

| 5 | $56,275 | $45,000 | 20.04% |

| 6 | $57,964 | $45,000 | 22.37% |

| 7 | $59,703 | $45,000 | 24.63% |

| 8 | $61,494 | $45,000 | 26.82% |

| 9 | $63,339 | $45,000 | 28.95% |

| 10 | $65,239 | $45,000 | 31.02% |

So, how much should you save per month?

We’ve gone through a lot of data, both in words and visualizations, can we break this down to a few key points?

- If you have a specific savings goal, it is easy to calculate how much to save.

- If you have a nonspecific savings goal, your best bet is to turn it into a specific savings goal, and then calculate that way.

- A 10% savings rate is a decent place to start and will put you above the median US citizen.

- Keeping down lifestyle inflation and increasing your savings rate as your income grows will allow your savings rate to increase, allowing you an earlier retirement.